The Senate Fiscal Agency released their latest report on Michigan's Economic Outlook and Budget Review on Dec. 21st, and in it, they lay out exactly what has happened to Michigan's economy in the past 10 years, how that relates to our budget difficulties now, as well as how it affects our revenue forecasts and employment outlook for the future. It's an interesting and at times blood-chilling read when you try to wrap your head around the fact that we just went through what can only be described as a tectonic shift to the foundation of Michigan's basic economy - and realize that the shock waves from that shift continue to this day, and will continue well into the future.

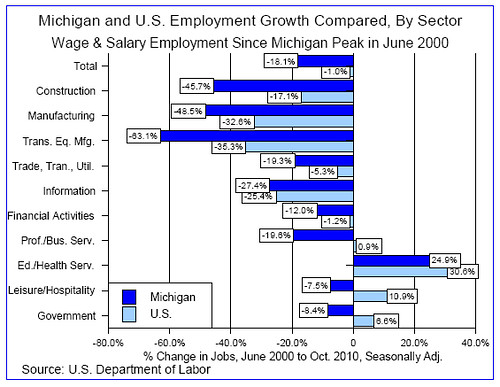

We entered the year 2000 a manufacturing state that was a 100 years in the making, and then we were hit with 10 years of severe contraction that was due to forces beyond our control. Here is the chart above, in their words:

Michigan's economy has spent the last 10 years in recession, largely driven by the same fundamental restructuring as that affecting manufacturing globally. Manufacturing has experienced a significant surge in productivity, driven by increased competition in the economy. For Michigan, the effect of productivity improvements was substantial, particularly given that there was more room for improvement in the durable goods and motor vehicle manufacturing sectors than in many other sectors, that Michigan is very disproportionately concentrated in motor vehicle manufacturing, and that the motor vehicle industries have become one of the most competitive sectors of the economy.

For Michigan, those factors were complicated as General Motors, Ford, and Chrysler lost market share over most of the last decade, leaving Michigan to lose employment from both productivity and reduced demand. The impact on the Michigan economy was exacerbated by the rapid and drastic decline in automobile sales in late 2008 and during 2009, reflecting national collapses in sectors such as construction, real estate, and finance.

When you see the word "productivity", think computers and robots and any other automation that has streamlined modern production and eliminated the need for humans to man those positions. It's the great unmentioned factor when it comes to job losses in manufacturing. And, when you add that to increased global competition, throw in the "most severe economic contraction in more than 70 years" during the Great Recession of 2008-09, and our economy being "very disproportionately concentrated in motor vehicle manufacturing", you end up with the chart above.

The SFA report indicates that the manufacturing job losses have stabilized, and are actually showing a slight increase at this point...

However, the drag from the manufacturing sector on Michigan's economy appears to have bottomed out and the recovery in vehicle sales nationally has helped Michigan's economic situation. Manufacturing employment in Michigan rose by 33,100 jobs (7.6%) between June 2009, when the U.S. recession ended, and October 2010. Employment in the transportation equipment manufacturing sector increased by 18.2% over that period, accounting for 20,000 of the manufacturing jobs Michigan gained. Michigan payroll employment declined for 12 consecutive months between July 2008 and June 2009, but has risen in seven of the last 16 months (with manufacturing employment rising in nine of the last 19 months). The unemployment rate declined from a high of 14.5% in December 2009 to 12.8% in October 2010, although a portion of that decline represents the departure of individuals from the labor force.

... and note the part about Michigan's performance in the past decade as it relates to other states.

While over the last 10 years Michigan's employment situation has fared worse than the national average, and, in some cases or time periods within that range, worse than any other state, Michigan's performance is not particularly inconsistent with other states when Michigan's economic composition is considered. Generally, states with higher manufacturing concentrations (particularly in the transportation equipment manufacturing sector) have experienced weaker job performance over the last 10 years, both because of the economic changes occurring in that sector and because of the dependence of other sectors within those states on manufacturing activity. As indicated earlier, productivity gains have made American manufacturing firms more profitable and more competitive, but have reduced the need for hiring additional employees to meet increased demand.

What does all this mean for the future, both immediate and long-term? It means that, although we still are tied to the domestic auto industry and manufacturing and we should continue to work on growing those industries - the old Michigan economy is never coming back.

Weak markets for housing, credit, and employment, coupled with high energy prices and substantial debt burdens, are expected to exert a dragging force on any increases in demand over the forecast period. Vehicle sales are expected to remain substantially below the levels experienced over the last two decades, although the Detroit 3 share of the sales mix is expected to remain fairly stable. Michigan's economic fortunes historically have been very closely linked with sales of domestically produced light vehicles. Despite the improvement forecasted in vehicle sales, and the renewed profitability of domestic automobile manufacturers, much of the additional demand can be met with existing employees and the low cost of capital means there will be few incentives to increase hiring significantly. As a result, although as of October 2010, Michigan had lost nearly two-thirds of the jobs (63.1%, a decline of nearly 223,100 jobs) in transportation equipment manufacturing that existed during the peak in July 2000, the majority of those jobs will never return and any gains in employment in the near future are likely to be muted. As identified in versions of this report prepared for earlier forecasts, even with something approximating normal employment growth in Michigan, it is unlikely that Michigan will reach the level of employment reported in June 2000 again until some time near the year 2035.

2035. And funny how "business taxes" never enter the conversation when it comes to job losses or forecasted job growth, isn't it?

Also note from the chart above that the job growth we have seen in Michigan in the past decade has been in education and health care, the latter having overtaken manufacturing as our number one employment sector. Unfortunately, those are the very areas that will likely face job losses in the next few years should the Republicans follow through with their plans to cut-off aid to state budgets at the national level, cut business tax revenue at the state level, and also try and deal with a FY 2011-12 budget deficit that is now estimated to be in the range of $1.85 billion - with no help coming in the foreseeable future. And, while they may claim that lower taxes will increase hiring, evidence shows that just isn't true. As a result, we are probably looking at severe cuts to services that will only exacerbate job loss in Michigan.

We still have a mountain ahead of us, Michigan, and the road looks rocky ahead, given that certain factions still stubbornly cling to the notion that wage reductions and more tax cuts will somehow bring us prosperity - but at least we know now where we have been.

Eventually, we will learn the lessons from this past decade. It just may take a little longer than we think.